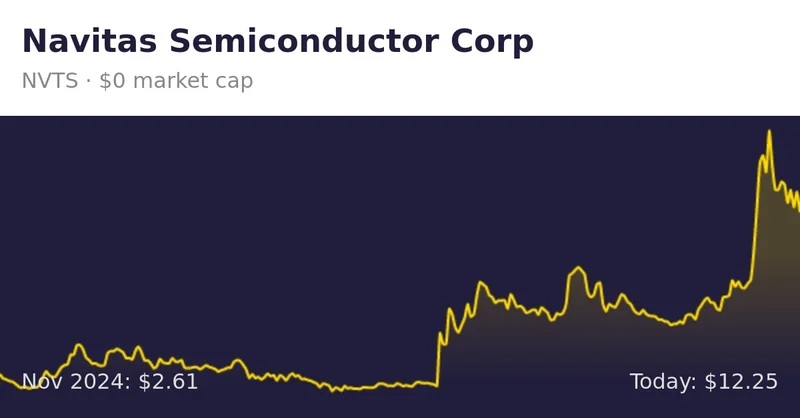

Navitas Semiconductor (NASDAQ:NVTS) just dropped its Q3 earnings, and the market's reaction was… less than enthusiastic. The stock took an 11.27% hit in after-hours trading, landing at $10.87. The headline? Revenue of $10.11 million, which, yes, technically beat analyst expectations of $10.01 million. But before we start popping champagne, let's dig a little deeper.

The problem isn’t the beat; it's the outlook. Navitas is projecting Q4 revenue between $6.75 million and $7.25 million. Analysts were expecting $10.05 million. That's not just a miss; it's a concerning discrepancy. What’s the story here?

Navitas is blaming the soft guidance on a strategic shift. They're deprioritizing their low-power China mobile and consumer business to focus on higher-power applications like AI data centers and energy infrastructure. The official line is that this is about chasing higher profits and bigger customers. Okay, makes sense on paper. But is it really that simple?

CEO Chris Allexandre talks about "accelerating demand" and Navitas' "decade-long technology leadership" in gallium nitride (GaN) and silicon carbide (SiC). Sounds great, right? Except, the numbers tell a slightly different story. Total revenue is down from $21.7 million year-over-year. That's a significant drop, not exactly the kind of "acceleration" you'd expect from a company supposedly riding the wave of global megatrends. I've looked at enough of these reports to know that sometimes, a "strategic shift" is just a fancy way of saying "we messed up." Navitas Semiconductor Stock Dives On Q3 Earnings, Soft Guidance - Navitas Semiconductor (NASDAQ:NVTS)

The company ended the quarter with $150.6 million in cash and equivalents. That's a decent cushion, but how long will it last if revenue continues to decline? And here's the part of the report that I find genuinely puzzling: if demand is truly accelerating, why the need to deprioritize anything? Shouldn't they be scaling up across all segments to meet this supposed surge?

This raises a crucial question about the company's internal forecasting: How accurate are their projections, and what assumptions are they based on? It's possible that Navitas is playing the long game, sacrificing short-term gains for long-term dominance in the high-power market. But that requires flawless execution and a truly differentiated product. Are they that far ahead of the competition?

Navitas is betting big on GaN and SiC. These materials offer advantages in terms of efficiency and power density. But they're also more expensive than traditional silicon. The key question is whether the performance benefits justify the higher cost, particularly in price-sensitive markets.

Think of it like this: GaN and SiC are like premium gasoline. They can boost performance, but only if the engine (the application) is designed to take advantage of their unique properties. If you're just using them in a standard engine (low-power consumer devices), you're not getting the full benefit, and you're paying a premium for nothing.

Navitas seems to be realizing this, hence the shift to high-power applications. But the high-power market is also becoming increasingly competitive. Established players like Infineon and STMicroelectronics are also investing heavily in GaN and SiC. Can Navitas maintain its "decade-long technology leadership" in the face of this competition? And more importantly, can they translate that leadership into sustainable revenue growth?

The problem is, with the limited information available, it’s hard to know whether the shift to higher power applications is a genuine strategic move, or a necessary correction to compensate for weakness in their original target markets. And what happens if the high-power market doesn't materialize as quickly as they expect?